In each The Submit and the Herald this morning there are experiences of interviews with govt members of the Reserve Financial institution’s Financial Coverage Committee: the Financial institution’s chief economist Paul Conway in The Submit and his boss, and the deputy chief govt chargeable for financial coverage and macroeconomics, Karen Silk within the Herald. In a high-performing central financial institution the holders of those two positions must be the folks we glance to for probably the most depth and authoritative background touch upon financial coverage and financial developments. However in New Zealand we’re coping with the legacy of the Orr/Quigley years the place we wrestle to get straightforwardness, not to mention depth and perception.

Now, to bend over backwards to be truthful, interview responses will rely, at the very least partially, on what the journalist involved chooses to ask. However then customary media coaching recommendation is to reply the query you would like they’d ask, not (essentially or solely simply) the one they did. An interview with a robust decisionmaker is a platform for the decisionmaker.

The Conway interview seems considerably meandering and never very centered. I wished to the touch on three units of feedback in it.

First, requested in regards to the transition after Adrian Orr’s sudden (and unexplained) departure, he says it’s enterprise as ordinary and it has been “a really clean transition”.

“I feel this establishment is larger than even Adrian Orr [it was certainly bigger – much bigger – as a result of Adrian Orr]……There’s an actual sense of the ‘present should go on’ and it actually has. We miss Adrian. It’s a bit much less enjoyable across the place, much less jokes occurring – most likely extra applicable jokes”, he smiles once more.

So along with Orr being a bully, an empire builder, and somebody well-known for freezing out problem and dissent, he additionally created an uncomfortable and inappropriate working atmosphere? Or at the very least that’s what Conway seems to be saying in regards to the man who recruited him.

However you additionally surprise about simply how straight Conway is being (and why the journalist didn’t ask extra). In spite of everything, the Financial institution itself tells us there are huge adjustments afoot (presumably consequent on the brand new Funding Settlement, prospect and precise). Within the simply over two months since Orr resigned, the highest tier of administration has been brutally slimmed down (credit score to Hawkesby). At first of March there was the Governor and an Govt Management Staff of seven Assistant/Deputy Governors and one “Strategic Adviser”. Since then, Kate Kolich, Greg Smith, Sarah Owen, Simone Robbers and Nigel Prince have all both left already or we’ve been suggested they’ll quickly be doing so (none with an introduced job to go to). Governor plus eight has been decreased to Governor plus 4. And

That first group is Conway’s personal stage (although presumably the Financial institution will proceed to want a chief economist). After which on right down to the employees (and far of it is because Orr/Quigley massively blew the funds restrict Grant Robertson had set for them and went on one final hiring spree final 12 months). You in some way suspect that every one shouldn’t be precisely sweetness, gentle, and engagement on the Reserve Financial institution.

After which there was this

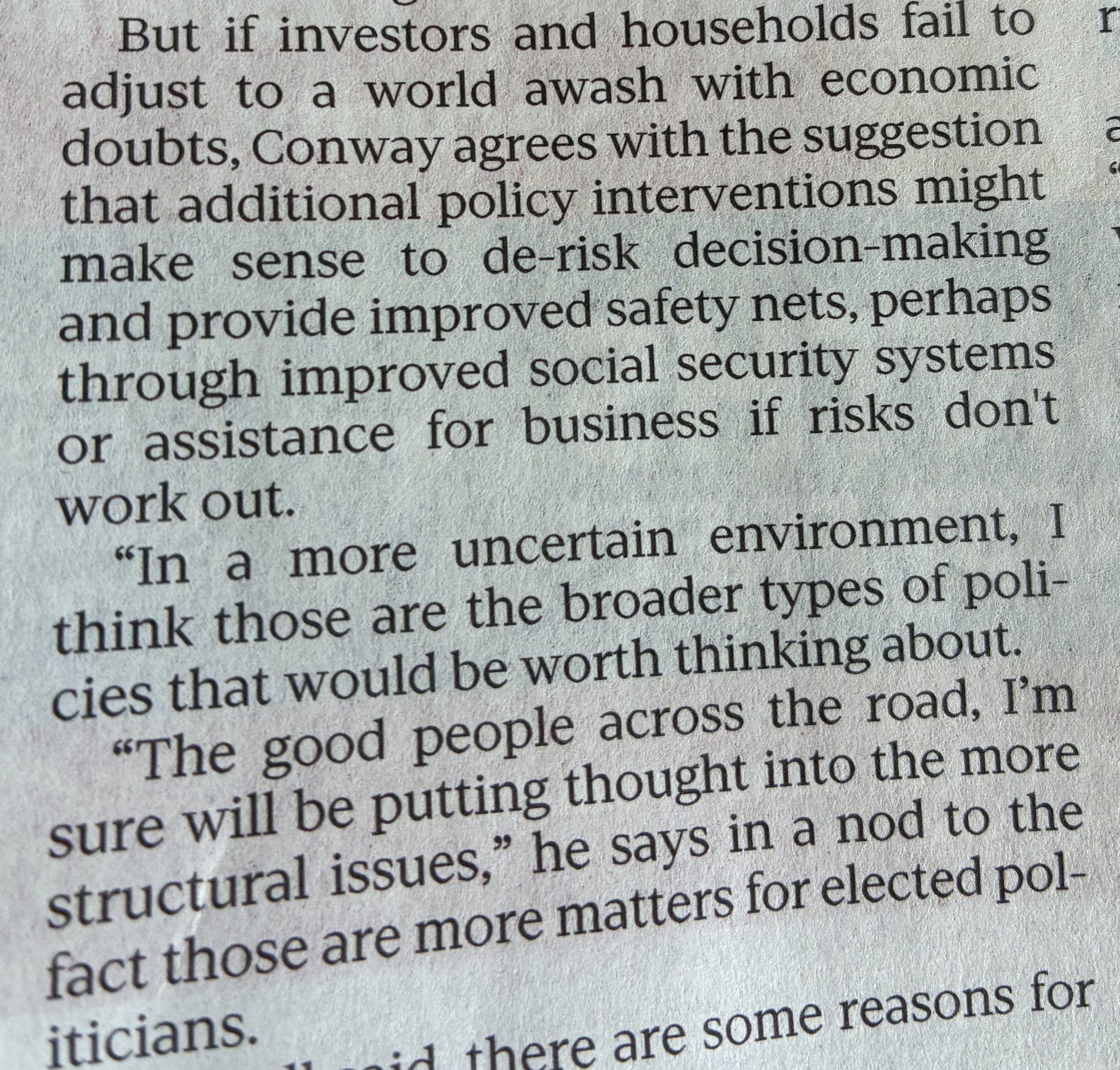

Conway is on file as a bigger-government form of man (we had his extra-curricular stuff final 12 months, for instance) however what possessed him, interviewed as an MPC member and senior central banker, to recommend that extra state interventions and greater authorities is perhaps “value fascinated by”? It merely isn’t in his bailiwick, and he shouldn’t have allowed himself to be dragged into responding to a hypothetical, particularly about one outdoors the Financial institution’s obligations.

And eventually, we obtained the meandering thought that “it’s potential that we get to some extent the place folks simply regulate their behaviours and ‘uncertainty’ turns into the brand new regular and we simply get on with it. I’ve obtained no ’empirics’ to base that on – it’s simply, I feel, a really fascinating thought-stream.”

Actually? A “very fascinating thought-stream” that individuals do actually adapt to the world as it’s? Startling and insightful (not).

Then, after all, there’s his boss, Silk. Most severe observers regard her as essentially unqualified for her job, and never the form of one that can be prone to be on an MPC anyplace else on this planet, not to mention because the deputy primarily chargeable for financial coverage. She might be counted on to securely ship speeches on operational subjects that others have written for her, and to reply purely factual questions at MPS press conferences and FEC about what has occurred to swap yields and mortgage charges. And that’s about all.

She additionally appears to have a mindset through which charges being paid on current mortgages are what matter moderately than the charges going through marginal debtors and purchasers. Maybe it’s what comes from a non-economics background in a financial institution? Thus, within the Herald interview we’re advised that she claimed that “the consequences of the 225 foundation factors of OCR cuts the committee had delivered in lower than a 12 months had been but to be broadly felt”. The journalist added some RB knowledge on common precise mortgage charges which could seem to again that up. In fact, anticipated money flows matter in addition to precise ones – in case your mounted fee mortgage goes to roll over in a few months onto a a lot decrease fee that may nearly actually be affecting your consolation, confidence, and willingness to spend now. However extra to the purpose, marginal charges for folks looking to buy a property or in any other case taking up new debt have come down a good distance, and had been already down a good distance months in the past. This chart is from the Financial institution’s personal web site, exhibiting short-term mounted mortgage charges.

As at yesterday, charges had been just a few foundation factors decrease once more than the end-April charges proven right here. 200 foundation factors plus down from the height, and that not simply yesterday. And falling wholesale charges, which underpin these falls in retail charges, additionally have an effect on the trade fee, one other necessary a part of the transmission mechanism. (And, after all, with all Silk’s give attention to the money flows of current debtors, she by no means ever mentions the offsetting adjustments within the money flows for current depositors – I’m of an age to know!)

Up to now, so predictable (at the very least from Silk). However then there was this (charitably I’ll assume the phrase “fulsome” was not hers)

Affordable folks would possibly differ over the inflation outlook and the required future path for the OCR, besides that we had been advised within the MPS that there was unanimous settlement from the MPC to the forecast path for rates of interest. And that may be a path that’s decrease from right here than the trail printed (once more unanimously) within the February MPS (the deviation begins after the Might MPS, not at it). In different phrases, not solely did the February path present some additional easing from (the place they anticipated to be, and had been, by) Might onwards, however the Might path reveals much more easing from right here ahead.

And but Silk talks of a “a lot stronger easing sign” despatched in February.

Frankly, they appear all over. If the Committee (because it did) unanimously agrees to publish a (considerably) steeper downward monitor than the one you had earlier than then both you could have an easing bias – all the time contingent on the information after all – otherwise you made a mistake in adopting the monitor you probably did. And in case you are snug with the monitor, it seems like a mis-step for the short-term fill-in Governor to announce that there was no bias. I suppose Silk may need obtained caught having to cowl for her fill-in boss, however it’s a fairly poor look all spherical. Certainly (certainly?) they should have rehearsed strains about biases earlier than the press convention? Certainly, in that case, somebody identified the disconnect between the proposed phrases and the chart above?

And eventually from Silk we study that “value stability is among the situations you want for progress”. It merely isn’t – and the economists on the committee are normally far more cautious, with the usual central banker line being that value stability, or low and steady inflation, is the perfect contribution financial coverage could make (many muttering beneath their breath that that contribution isn’t essentially very massive). To not labour the purpose however the financial system was nonetheless rising, reaching its most overheated level in late 2022, when core inflation was round its worst.

All in all, not a terrific effort at communications from the MPC this week. As I famous in my put up on Thursday, there was not one of the prickly frostiness of Orr, and no signal of intentionally or acutely aware getting down to mislead Parliament, nevertheless it merely wasn’t an excellent efficiency. And whereas Hawkesby is new to the position, chairing MPC and performing as its prime spokesperson on the day, Conway and Silk haven’t any such excuse. Somebody flippantly recommended that maybe there’s something about Might and the MPC – final Might was when the MPC went a bit wild speaking of elevating charges additional (the OCR was nonetheless going to be above 5 per cent by now), after which Conway tried in charge his instruments, moderately than the judgements of him and his colleagues, for the related forecasts.

If the federal government is in any respect severe a couple of a lot better, world class, Reserve Financial institution, they should work with the Board to discover a Governor who will carry the sport and the Governor/refreshed Board might want to work with the Minister to supply a stronger MPC. It might appear unlikely that in such an improved Financial institution/MPC there can be a pure place for both Conway or Silk, nice sufficient folks as they might be.

In each The Submit and the Herald this morning there are experiences of interviews with govt members of the Reserve Financial institution’s Financial Coverage Committee: the Financial institution’s chief economist Paul Conway in The Submit and his boss, and the deputy chief govt chargeable for financial coverage and macroeconomics, Karen Silk within the Herald. In a high-performing central financial institution the holders of those two positions must be the folks we glance to for probably the most depth and authoritative background touch upon financial coverage and financial developments. However in New Zealand we’re coping with the legacy of the Orr/Quigley years the place we wrestle to get straightforwardness, not to mention depth and perception.

Now, to bend over backwards to be truthful, interview responses will rely, at the very least partially, on what the journalist involved chooses to ask. However then customary media coaching recommendation is to reply the query you would like they’d ask, not (essentially or solely simply) the one they did. An interview with a robust decisionmaker is a platform for the decisionmaker.

The Conway interview seems considerably meandering and never very centered. I wished to the touch on three units of feedback in it.

First, requested in regards to the transition after Adrian Orr’s sudden (and unexplained) departure, he says it’s enterprise as ordinary and it has been “a really clean transition”.

“I feel this establishment is larger than even Adrian Orr [it was certainly bigger – much bigger – as a result of Adrian Orr]……There’s an actual sense of the ‘present should go on’ and it actually has. We miss Adrian. It’s a bit much less enjoyable across the place, much less jokes occurring – most likely extra applicable jokes”, he smiles once more.

So along with Orr being a bully, an empire builder, and somebody well-known for freezing out problem and dissent, he additionally created an uncomfortable and inappropriate working atmosphere? Or at the very least that’s what Conway seems to be saying in regards to the man who recruited him.

However you additionally surprise about simply how straight Conway is being (and why the journalist didn’t ask extra). In spite of everything, the Financial institution itself tells us there are huge adjustments afoot (presumably consequent on the brand new Funding Settlement, prospect and precise). Within the simply over two months since Orr resigned, the highest tier of administration has been brutally slimmed down (credit score to Hawkesby). At first of March there was the Governor and an Govt Management Staff of seven Assistant/Deputy Governors and one “Strategic Adviser”. Since then, Kate Kolich, Greg Smith, Sarah Owen, Simone Robbers and Nigel Prince have all both left already or we’ve been suggested they’ll quickly be doing so (none with an introduced job to go to). Governor plus eight has been decreased to Governor plus 4. And

That first group is Conway’s personal stage (although presumably the Financial institution will proceed to want a chief economist). After which on right down to the employees (and far of it is because Orr/Quigley massively blew the funds restrict Grant Robertson had set for them and went on one final hiring spree final 12 months). You in some way suspect that every one shouldn’t be precisely sweetness, gentle, and engagement on the Reserve Financial institution.

After which there was this

Conway is on file as a bigger-government form of man (we had his extra-curricular stuff final 12 months, for instance) however what possessed him, interviewed as an MPC member and senior central banker, to recommend that extra state interventions and greater authorities is perhaps “value fascinated by”? It merely isn’t in his bailiwick, and he shouldn’t have allowed himself to be dragged into responding to a hypothetical, particularly about one outdoors the Financial institution’s obligations.

And eventually, we obtained the meandering thought that “it’s potential that we get to some extent the place folks simply regulate their behaviours and ‘uncertainty’ turns into the brand new regular and we simply get on with it. I’ve obtained no ’empirics’ to base that on – it’s simply, I feel, a really fascinating thought-stream.”

Actually? A “very fascinating thought-stream” that individuals do actually adapt to the world as it’s? Startling and insightful (not).

Then, after all, there’s his boss, Silk. Most severe observers regard her as essentially unqualified for her job, and never the form of one that can be prone to be on an MPC anyplace else on this planet, not to mention because the deputy primarily chargeable for financial coverage. She might be counted on to securely ship speeches on operational subjects that others have written for her, and to reply purely factual questions at MPS press conferences and FEC about what has occurred to swap yields and mortgage charges. And that’s about all.

She additionally appears to have a mindset through which charges being paid on current mortgages are what matter moderately than the charges going through marginal debtors and purchasers. Maybe it’s what comes from a non-economics background in a financial institution? Thus, within the Herald interview we’re advised that she claimed that “the consequences of the 225 foundation factors of OCR cuts the committee had delivered in lower than a 12 months had been but to be broadly felt”. The journalist added some RB knowledge on common precise mortgage charges which could seem to again that up. In fact, anticipated money flows matter in addition to precise ones – in case your mounted fee mortgage goes to roll over in a few months onto a a lot decrease fee that may nearly actually be affecting your consolation, confidence, and willingness to spend now. However extra to the purpose, marginal charges for folks looking to buy a property or in any other case taking up new debt have come down a good distance, and had been already down a good distance months in the past. This chart is from the Financial institution’s personal web site, exhibiting short-term mounted mortgage charges.

As at yesterday, charges had been just a few foundation factors decrease once more than the end-April charges proven right here. 200 foundation factors plus down from the height, and that not simply yesterday. And falling wholesale charges, which underpin these falls in retail charges, additionally have an effect on the trade fee, one other necessary a part of the transmission mechanism. (And, after all, with all Silk’s give attention to the money flows of current debtors, she by no means ever mentions the offsetting adjustments within the money flows for current depositors – I’m of an age to know!)

Up to now, so predictable (at the very least from Silk). However then there was this (charitably I’ll assume the phrase “fulsome” was not hers)

Affordable folks would possibly differ over the inflation outlook and the required future path for the OCR, besides that we had been advised within the MPS that there was unanimous settlement from the MPC to the forecast path for rates of interest. And that may be a path that’s decrease from right here than the trail printed (once more unanimously) within the February MPS (the deviation begins after the Might MPS, not at it). In different phrases, not solely did the February path present some additional easing from (the place they anticipated to be, and had been, by) Might onwards, however the Might path reveals much more easing from right here ahead.

And but Silk talks of a “a lot stronger easing sign” despatched in February.

Frankly, they appear all over. If the Committee (because it did) unanimously agrees to publish a (considerably) steeper downward monitor than the one you had earlier than then both you could have an easing bias – all the time contingent on the information after all – otherwise you made a mistake in adopting the monitor you probably did. And in case you are snug with the monitor, it seems like a mis-step for the short-term fill-in Governor to announce that there was no bias. I suppose Silk may need obtained caught having to cowl for her fill-in boss, however it’s a fairly poor look all spherical. Certainly (certainly?) they should have rehearsed strains about biases earlier than the press convention? Certainly, in that case, somebody identified the disconnect between the proposed phrases and the chart above?

And eventually from Silk we study that “value stability is among the situations you want for progress”. It merely isn’t – and the economists on the committee are normally far more cautious, with the usual central banker line being that value stability, or low and steady inflation, is the perfect contribution financial coverage could make (many muttering beneath their breath that that contribution isn’t essentially very massive). To not labour the purpose however the financial system was nonetheless rising, reaching its most overheated level in late 2022, when core inflation was round its worst.

All in all, not a terrific effort at communications from the MPC this week. As I famous in my put up on Thursday, there was not one of the prickly frostiness of Orr, and no signal of intentionally or acutely aware getting down to mislead Parliament, nevertheless it merely wasn’t an excellent efficiency. And whereas Hawkesby is new to the position, chairing MPC and performing as its prime spokesperson on the day, Conway and Silk haven’t any such excuse. Somebody flippantly recommended that maybe there’s something about Might and the MPC – final Might was when the MPC went a bit wild speaking of elevating charges additional (the OCR was nonetheless going to be above 5 per cent by now), after which Conway tried in charge his instruments, moderately than the judgements of him and his colleagues, for the related forecasts.

If the federal government is in any respect severe a couple of a lot better, world class, Reserve Financial institution, they should work with the Board to discover a Governor who will carry the sport and the Governor/refreshed Board might want to work with the Minister to supply a stronger MPC. It might appear unlikely that in such an improved Financial institution/MPC there can be a pure place for both Conway or Silk, nice sufficient folks as they might be.

In each The Submit and the Herald this morning there are experiences of interviews with govt members of the Reserve Financial institution’s Financial Coverage Committee: the Financial institution’s chief economist Paul Conway in The Submit and his boss, and the deputy chief govt chargeable for financial coverage and macroeconomics, Karen Silk within the Herald. In a high-performing central financial institution the holders of those two positions must be the folks we glance to for probably the most depth and authoritative background touch upon financial coverage and financial developments. However in New Zealand we’re coping with the legacy of the Orr/Quigley years the place we wrestle to get straightforwardness, not to mention depth and perception.

Now, to bend over backwards to be truthful, interview responses will rely, at the very least partially, on what the journalist involved chooses to ask. However then customary media coaching recommendation is to reply the query you would like they’d ask, not (essentially or solely simply) the one they did. An interview with a robust decisionmaker is a platform for the decisionmaker.

The Conway interview seems considerably meandering and never very centered. I wished to the touch on three units of feedback in it.

First, requested in regards to the transition after Adrian Orr’s sudden (and unexplained) departure, he says it’s enterprise as ordinary and it has been “a really clean transition”.

“I feel this establishment is larger than even Adrian Orr [it was certainly bigger – much bigger – as a result of Adrian Orr]……There’s an actual sense of the ‘present should go on’ and it actually has. We miss Adrian. It’s a bit much less enjoyable across the place, much less jokes occurring – most likely extra applicable jokes”, he smiles once more.

So along with Orr being a bully, an empire builder, and somebody well-known for freezing out problem and dissent, he additionally created an uncomfortable and inappropriate working atmosphere? Or at the very least that’s what Conway seems to be saying in regards to the man who recruited him.

However you additionally surprise about simply how straight Conway is being (and why the journalist didn’t ask extra). In spite of everything, the Financial institution itself tells us there are huge adjustments afoot (presumably consequent on the brand new Funding Settlement, prospect and precise). Within the simply over two months since Orr resigned, the highest tier of administration has been brutally slimmed down (credit score to Hawkesby). At first of March there was the Governor and an Govt Management Staff of seven Assistant/Deputy Governors and one “Strategic Adviser”. Since then, Kate Kolich, Greg Smith, Sarah Owen, Simone Robbers and Nigel Prince have all both left already or we’ve been suggested they’ll quickly be doing so (none with an introduced job to go to). Governor plus eight has been decreased to Governor plus 4. And

That first group is Conway’s personal stage (although presumably the Financial institution will proceed to want a chief economist). After which on right down to the employees (and far of it is because Orr/Quigley massively blew the funds restrict Grant Robertson had set for them and went on one final hiring spree final 12 months). You in some way suspect that every one shouldn’t be precisely sweetness, gentle, and engagement on the Reserve Financial institution.

After which there was this

Conway is on file as a bigger-government form of man (we had his extra-curricular stuff final 12 months, for instance) however what possessed him, interviewed as an MPC member and senior central banker, to recommend that extra state interventions and greater authorities is perhaps “value fascinated by”? It merely isn’t in his bailiwick, and he shouldn’t have allowed himself to be dragged into responding to a hypothetical, particularly about one outdoors the Financial institution’s obligations.

And eventually, we obtained the meandering thought that “it’s potential that we get to some extent the place folks simply regulate their behaviours and ‘uncertainty’ turns into the brand new regular and we simply get on with it. I’ve obtained no ’empirics’ to base that on – it’s simply, I feel, a really fascinating thought-stream.”

Actually? A “very fascinating thought-stream” that individuals do actually adapt to the world as it’s? Startling and insightful (not).

Then, after all, there’s his boss, Silk. Most severe observers regard her as essentially unqualified for her job, and never the form of one that can be prone to be on an MPC anyplace else on this planet, not to mention because the deputy primarily chargeable for financial coverage. She might be counted on to securely ship speeches on operational subjects that others have written for her, and to reply purely factual questions at MPS press conferences and FEC about what has occurred to swap yields and mortgage charges. And that’s about all.

She additionally appears to have a mindset through which charges being paid on current mortgages are what matter moderately than the charges going through marginal debtors and purchasers. Maybe it’s what comes from a non-economics background in a financial institution? Thus, within the Herald interview we’re advised that she claimed that “the consequences of the 225 foundation factors of OCR cuts the committee had delivered in lower than a 12 months had been but to be broadly felt”. The journalist added some RB knowledge on common precise mortgage charges which could seem to again that up. In fact, anticipated money flows matter in addition to precise ones – in case your mounted fee mortgage goes to roll over in a few months onto a a lot decrease fee that may nearly actually be affecting your consolation, confidence, and willingness to spend now. However extra to the purpose, marginal charges for folks looking to buy a property or in any other case taking up new debt have come down a good distance, and had been already down a good distance months in the past. This chart is from the Financial institution’s personal web site, exhibiting short-term mounted mortgage charges.

As at yesterday, charges had been just a few foundation factors decrease once more than the end-April charges proven right here. 200 foundation factors plus down from the height, and that not simply yesterday. And falling wholesale charges, which underpin these falls in retail charges, additionally have an effect on the trade fee, one other necessary a part of the transmission mechanism. (And, after all, with all Silk’s give attention to the money flows of current debtors, she by no means ever mentions the offsetting adjustments within the money flows for current depositors – I’m of an age to know!)

Up to now, so predictable (at the very least from Silk). However then there was this (charitably I’ll assume the phrase “fulsome” was not hers)

Affordable folks would possibly differ over the inflation outlook and the required future path for the OCR, besides that we had been advised within the MPS that there was unanimous settlement from the MPC to the forecast path for rates of interest. And that may be a path that’s decrease from right here than the trail printed (once more unanimously) within the February MPS (the deviation begins after the Might MPS, not at it). In different phrases, not solely did the February path present some additional easing from (the place they anticipated to be, and had been, by) Might onwards, however the Might path reveals much more easing from right here ahead.

And but Silk talks of a “a lot stronger easing sign” despatched in February.

Frankly, they appear all over. If the Committee (because it did) unanimously agrees to publish a (considerably) steeper downward monitor than the one you had earlier than then both you could have an easing bias – all the time contingent on the information after all – otherwise you made a mistake in adopting the monitor you probably did. And in case you are snug with the monitor, it seems like a mis-step for the short-term fill-in Governor to announce that there was no bias. I suppose Silk may need obtained caught having to cowl for her fill-in boss, however it’s a fairly poor look all spherical. Certainly (certainly?) they should have rehearsed strains about biases earlier than the press convention? Certainly, in that case, somebody identified the disconnect between the proposed phrases and the chart above?

And eventually from Silk we study that “value stability is among the situations you want for progress”. It merely isn’t – and the economists on the committee are normally far more cautious, with the usual central banker line being that value stability, or low and steady inflation, is the perfect contribution financial coverage could make (many muttering beneath their breath that that contribution isn’t essentially very massive). To not labour the purpose however the financial system was nonetheless rising, reaching its most overheated level in late 2022, when core inflation was round its worst.

All in all, not a terrific effort at communications from the MPC this week. As I famous in my put up on Thursday, there was not one of the prickly frostiness of Orr, and no signal of intentionally or acutely aware getting down to mislead Parliament, nevertheless it merely wasn’t an excellent efficiency. And whereas Hawkesby is new to the position, chairing MPC and performing as its prime spokesperson on the day, Conway and Silk haven’t any such excuse. Somebody flippantly recommended that maybe there’s something about Might and the MPC – final Might was when the MPC went a bit wild speaking of elevating charges additional (the OCR was nonetheless going to be above 5 per cent by now), after which Conway tried in charge his instruments, moderately than the judgements of him and his colleagues, for the related forecasts.

If the federal government is in any respect severe a couple of a lot better, world class, Reserve Financial institution, they should work with the Board to discover a Governor who will carry the sport and the Governor/refreshed Board might want to work with the Minister to supply a stronger MPC. It might appear unlikely that in such an improved Financial institution/MPC there can be a pure place for both Conway or Silk, nice sufficient folks as they might be.

In each The Submit and the Herald this morning there are experiences of interviews with govt members of the Reserve Financial institution’s Financial Coverage Committee: the Financial institution’s chief economist Paul Conway in The Submit and his boss, and the deputy chief govt chargeable for financial coverage and macroeconomics, Karen Silk within the Herald. In a high-performing central financial institution the holders of those two positions must be the folks we glance to for probably the most depth and authoritative background touch upon financial coverage and financial developments. However in New Zealand we’re coping with the legacy of the Orr/Quigley years the place we wrestle to get straightforwardness, not to mention depth and perception.

Now, to bend over backwards to be truthful, interview responses will rely, at the very least partially, on what the journalist involved chooses to ask. However then customary media coaching recommendation is to reply the query you would like they’d ask, not (essentially or solely simply) the one they did. An interview with a robust decisionmaker is a platform for the decisionmaker.

The Conway interview seems considerably meandering and never very centered. I wished to the touch on three units of feedback in it.

First, requested in regards to the transition after Adrian Orr’s sudden (and unexplained) departure, he says it’s enterprise as ordinary and it has been “a really clean transition”.

“I feel this establishment is larger than even Adrian Orr [it was certainly bigger – much bigger – as a result of Adrian Orr]……There’s an actual sense of the ‘present should go on’ and it actually has. We miss Adrian. It’s a bit much less enjoyable across the place, much less jokes occurring – most likely extra applicable jokes”, he smiles once more.

So along with Orr being a bully, an empire builder, and somebody well-known for freezing out problem and dissent, he additionally created an uncomfortable and inappropriate working atmosphere? Or at the very least that’s what Conway seems to be saying in regards to the man who recruited him.

However you additionally surprise about simply how straight Conway is being (and why the journalist didn’t ask extra). In spite of everything, the Financial institution itself tells us there are huge adjustments afoot (presumably consequent on the brand new Funding Settlement, prospect and precise). Within the simply over two months since Orr resigned, the highest tier of administration has been brutally slimmed down (credit score to Hawkesby). At first of March there was the Governor and an Govt Management Staff of seven Assistant/Deputy Governors and one “Strategic Adviser”. Since then, Kate Kolich, Greg Smith, Sarah Owen, Simone Robbers and Nigel Prince have all both left already or we’ve been suggested they’ll quickly be doing so (none with an introduced job to go to). Governor plus eight has been decreased to Governor plus 4. And

That first group is Conway’s personal stage (although presumably the Financial institution will proceed to want a chief economist). After which on right down to the employees (and far of it is because Orr/Quigley massively blew the funds restrict Grant Robertson had set for them and went on one final hiring spree final 12 months). You in some way suspect that every one shouldn’t be precisely sweetness, gentle, and engagement on the Reserve Financial institution.

After which there was this

Conway is on file as a bigger-government form of man (we had his extra-curricular stuff final 12 months, for instance) however what possessed him, interviewed as an MPC member and senior central banker, to recommend that extra state interventions and greater authorities is perhaps “value fascinated by”? It merely isn’t in his bailiwick, and he shouldn’t have allowed himself to be dragged into responding to a hypothetical, particularly about one outdoors the Financial institution’s obligations.

And eventually, we obtained the meandering thought that “it’s potential that we get to some extent the place folks simply regulate their behaviours and ‘uncertainty’ turns into the brand new regular and we simply get on with it. I’ve obtained no ’empirics’ to base that on – it’s simply, I feel, a really fascinating thought-stream.”

Actually? A “very fascinating thought-stream” that individuals do actually adapt to the world as it’s? Startling and insightful (not).

Then, after all, there’s his boss, Silk. Most severe observers regard her as essentially unqualified for her job, and never the form of one that can be prone to be on an MPC anyplace else on this planet, not to mention because the deputy primarily chargeable for financial coverage. She might be counted on to securely ship speeches on operational subjects that others have written for her, and to reply purely factual questions at MPS press conferences and FEC about what has occurred to swap yields and mortgage charges. And that’s about all.

She additionally appears to have a mindset through which charges being paid on current mortgages are what matter moderately than the charges going through marginal debtors and purchasers. Maybe it’s what comes from a non-economics background in a financial institution? Thus, within the Herald interview we’re advised that she claimed that “the consequences of the 225 foundation factors of OCR cuts the committee had delivered in lower than a 12 months had been but to be broadly felt”. The journalist added some RB knowledge on common precise mortgage charges which could seem to again that up. In fact, anticipated money flows matter in addition to precise ones – in case your mounted fee mortgage goes to roll over in a few months onto a a lot decrease fee that may nearly actually be affecting your consolation, confidence, and willingness to spend now. However extra to the purpose, marginal charges for folks looking to buy a property or in any other case taking up new debt have come down a good distance, and had been already down a good distance months in the past. This chart is from the Financial institution’s personal web site, exhibiting short-term mounted mortgage charges.

As at yesterday, charges had been just a few foundation factors decrease once more than the end-April charges proven right here. 200 foundation factors plus down from the height, and that not simply yesterday. And falling wholesale charges, which underpin these falls in retail charges, additionally have an effect on the trade fee, one other necessary a part of the transmission mechanism. (And, after all, with all Silk’s give attention to the money flows of current debtors, she by no means ever mentions the offsetting adjustments within the money flows for current depositors – I’m of an age to know!)

Up to now, so predictable (at the very least from Silk). However then there was this (charitably I’ll assume the phrase “fulsome” was not hers)

Affordable folks would possibly differ over the inflation outlook and the required future path for the OCR, besides that we had been advised within the MPS that there was unanimous settlement from the MPC to the forecast path for rates of interest. And that may be a path that’s decrease from right here than the trail printed (once more unanimously) within the February MPS (the deviation begins after the Might MPS, not at it). In different phrases, not solely did the February path present some additional easing from (the place they anticipated to be, and had been, by) Might onwards, however the Might path reveals much more easing from right here ahead.

And but Silk talks of a “a lot stronger easing sign” despatched in February.

Frankly, they appear all over. If the Committee (because it did) unanimously agrees to publish a (considerably) steeper downward monitor than the one you had earlier than then both you could have an easing bias – all the time contingent on the information after all – otherwise you made a mistake in adopting the monitor you probably did. And in case you are snug with the monitor, it seems like a mis-step for the short-term fill-in Governor to announce that there was no bias. I suppose Silk may need obtained caught having to cowl for her fill-in boss, however it’s a fairly poor look all spherical. Certainly (certainly?) they should have rehearsed strains about biases earlier than the press convention? Certainly, in that case, somebody identified the disconnect between the proposed phrases and the chart above?

And eventually from Silk we study that “value stability is among the situations you want for progress”. It merely isn’t – and the economists on the committee are normally far more cautious, with the usual central banker line being that value stability, or low and steady inflation, is the perfect contribution financial coverage could make (many muttering beneath their breath that that contribution isn’t essentially very massive). To not labour the purpose however the financial system was nonetheless rising, reaching its most overheated level in late 2022, when core inflation was round its worst.

All in all, not a terrific effort at communications from the MPC this week. As I famous in my put up on Thursday, there was not one of the prickly frostiness of Orr, and no signal of intentionally or acutely aware getting down to mislead Parliament, nevertheless it merely wasn’t an excellent efficiency. And whereas Hawkesby is new to the position, chairing MPC and performing as its prime spokesperson on the day, Conway and Silk haven’t any such excuse. Somebody flippantly recommended that maybe there’s something about Might and the MPC – final Might was when the MPC went a bit wild speaking of elevating charges additional (the OCR was nonetheless going to be above 5 per cent by now), after which Conway tried in charge his instruments, moderately than the judgements of him and his colleagues, for the related forecasts.

If the federal government is in any respect severe a couple of a lot better, world class, Reserve Financial institution, they should work with the Board to discover a Governor who will carry the sport and the Governor/refreshed Board might want to work with the Minister to supply a stronger MPC. It might appear unlikely that in such an improved Financial institution/MPC there can be a pure place for both Conway or Silk, nice sufficient folks as they might be.

{kind=link}