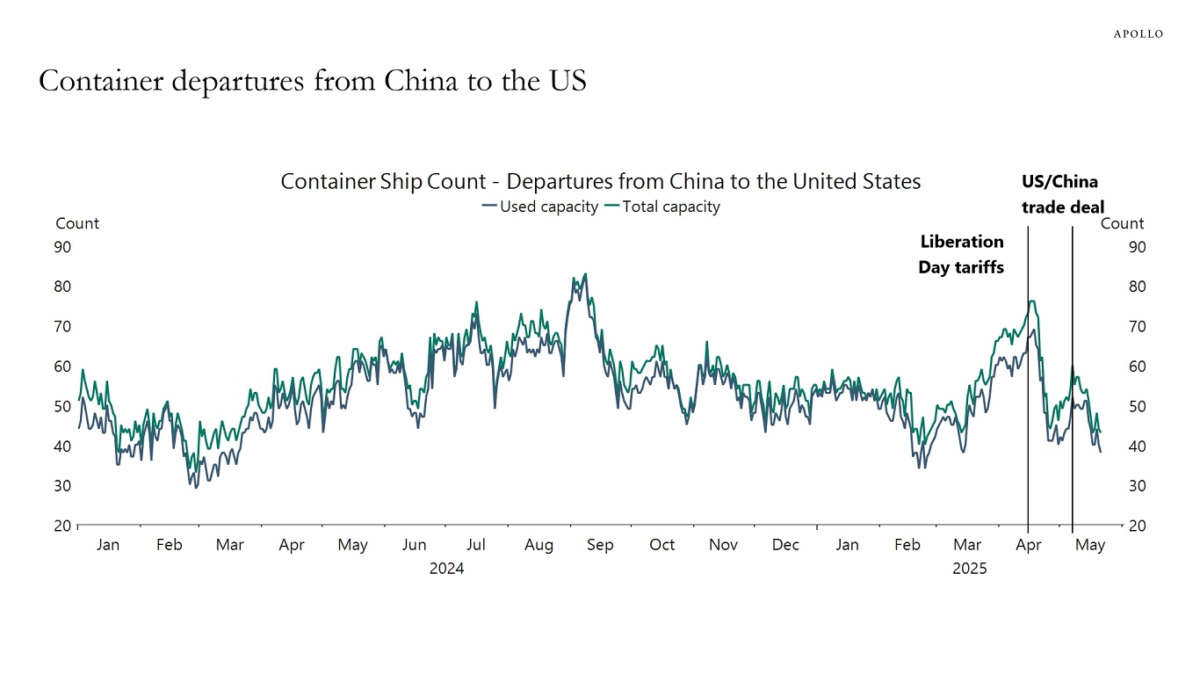

Extra precisely, nowcasted utilizing inbound container visitors. Two thirds of Chinese language imports (by worth) comes by sea freight. And sea freight from China doesn’t appear to be rebounding; from Torsten Slok:

Supply: Slok, Might 25, 2025.

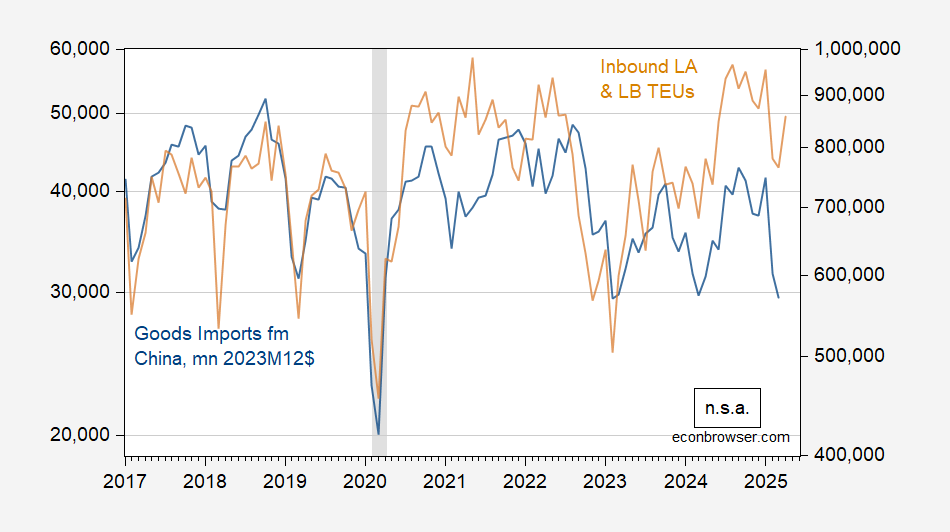

How are TEUs correlated with imports? Right here’s whole LA/Lengthy Seashore inbound TEUs and Chinese language imports (deflated into 2003M12$)

Determine 1: Items imports from China, mn 2003M12$, n.s.a (blue, left log scale), crammed inbound TEUs to LA and Lengthy Seashore ports, n.s.a. (tan, proper log scale). Nominal sequence deflated into actual utilizing deflator for imports of Chinese language items. NBER peak-to-trough recession dates shaded grey. Supply: BEA , BLS by way of FRED, Ports of LA, Lengthy Seashore, NBER and creator’s calculations.

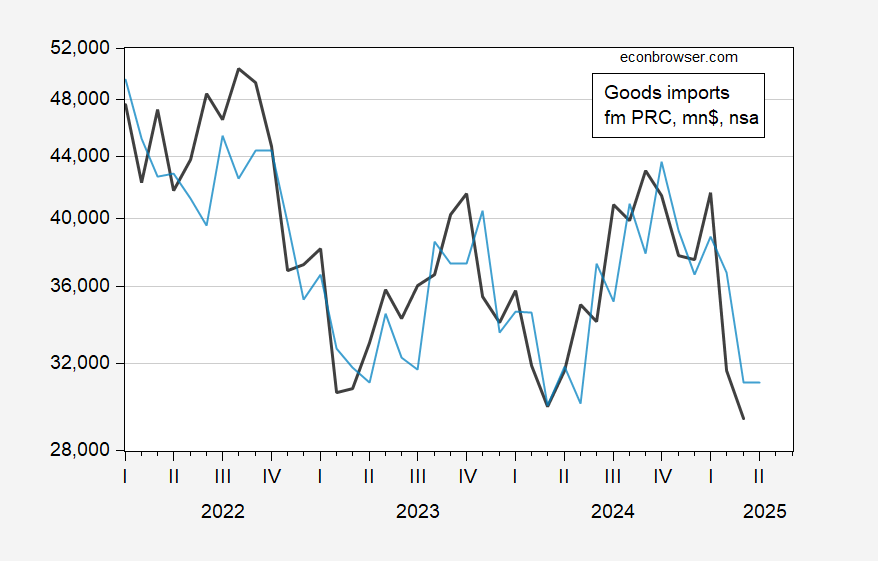

Can we predict April imports from China primarily based on inbound TEU’s? Over the 2022M01-2025M03 interval, I estimate in log first variations (utilizing not seasonally adjusted knowledge):

Δimpcht = -0.013 + 0.239 Δteu_LAt + 0.303Δteu_LBt + ut

Adj-R2 = 0.26, SER = 0.086, DW = 2.37, NObs = 39. Daring denotes important at 10% msl, utilizing Newey-West s.e.

Determine 2: Imports from China (black), and predicted imports utilizing indicated equation (mild blue), each in mn.2003M12$. Supply: BEA, BLS by way of FRED, and creator’s calculations.

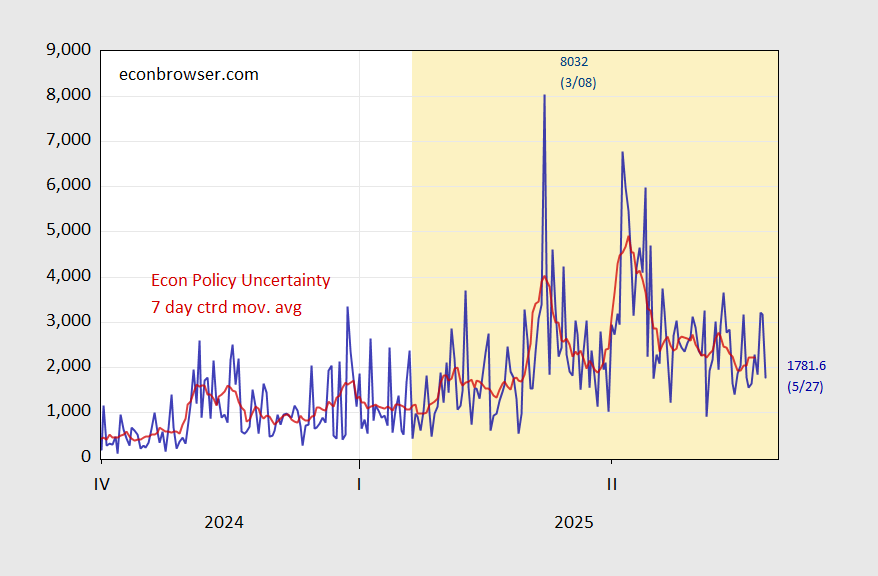

Ought to we anticipate a rebound now that there’s been an obvious pause in escalation within the commerce warfare with China. The primary determine supplied by Slok suggests no. And given the extremely fickle nature of Trump 2.0 commerce coverage, it’s comprehensible why that is the case.

Determine 3: EPU – commerce class (blue), 7-day centered transferring common (pink). Gentle orange shading signifies second Trump 2.0 administration. Supply: policyuncertainty.com.

For extra on nowcasting commerce utilizing (partially) container visitors, see this blogpost.

Extra precisely, nowcasted utilizing inbound container visitors. Two thirds of Chinese language imports (by worth) comes by sea freight. And sea freight from China doesn’t appear to be rebounding; from Torsten Slok:

Supply: Slok, Might 25, 2025.

How are TEUs correlated with imports? Right here’s whole LA/Lengthy Seashore inbound TEUs and Chinese language imports (deflated into 2003M12$)

Determine 1: Items imports from China, mn 2003M12$, n.s.a (blue, left log scale), crammed inbound TEUs to LA and Lengthy Seashore ports, n.s.a. (tan, proper log scale). Nominal sequence deflated into actual utilizing deflator for imports of Chinese language items. NBER peak-to-trough recession dates shaded grey. Supply: BEA , BLS by way of FRED, Ports of LA, Lengthy Seashore, NBER and creator’s calculations.

Can we predict April imports from China primarily based on inbound TEU’s? Over the 2022M01-2025M03 interval, I estimate in log first variations (utilizing not seasonally adjusted knowledge):

Δimpcht = -0.013 + 0.239 Δteu_LAt + 0.303Δteu_LBt + ut

Adj-R2 = 0.26, SER = 0.086, DW = 2.37, NObs = 39. Daring denotes important at 10% msl, utilizing Newey-West s.e.

Determine 2: Imports from China (black), and predicted imports utilizing indicated equation (mild blue), each in mn.2003M12$. Supply: BEA, BLS by way of FRED, and creator’s calculations.

Ought to we anticipate a rebound now that there’s been an obvious pause in escalation within the commerce warfare with China. The primary determine supplied by Slok suggests no. And given the extremely fickle nature of Trump 2.0 commerce coverage, it’s comprehensible why that is the case.

Determine 3: EPU – commerce class (blue), 7-day centered transferring common (pink). Gentle orange shading signifies second Trump 2.0 administration. Supply: policyuncertainty.com.

For extra on nowcasting commerce utilizing (partially) container visitors, see this blogpost.

Extra precisely, nowcasted utilizing inbound container visitors. Two thirds of Chinese language imports (by worth) comes by sea freight. And sea freight from China doesn’t appear to be rebounding; from Torsten Slok:

Supply: Slok, Might 25, 2025.

How are TEUs correlated with imports? Right here’s whole LA/Lengthy Seashore inbound TEUs and Chinese language imports (deflated into 2003M12$)

Determine 1: Items imports from China, mn 2003M12$, n.s.a (blue, left log scale), crammed inbound TEUs to LA and Lengthy Seashore ports, n.s.a. (tan, proper log scale). Nominal sequence deflated into actual utilizing deflator for imports of Chinese language items. NBER peak-to-trough recession dates shaded grey. Supply: BEA , BLS by way of FRED, Ports of LA, Lengthy Seashore, NBER and creator’s calculations.

Can we predict April imports from China primarily based on inbound TEU’s? Over the 2022M01-2025M03 interval, I estimate in log first variations (utilizing not seasonally adjusted knowledge):

Δimpcht = -0.013 + 0.239 Δteu_LAt + 0.303Δteu_LBt + ut

Adj-R2 = 0.26, SER = 0.086, DW = 2.37, NObs = 39. Daring denotes important at 10% msl, utilizing Newey-West s.e.

Determine 2: Imports from China (black), and predicted imports utilizing indicated equation (mild blue), each in mn.2003M12$. Supply: BEA, BLS by way of FRED, and creator’s calculations.

Ought to we anticipate a rebound now that there’s been an obvious pause in escalation within the commerce warfare with China. The primary determine supplied by Slok suggests no. And given the extremely fickle nature of Trump 2.0 commerce coverage, it’s comprehensible why that is the case.

Determine 3: EPU – commerce class (blue), 7-day centered transferring common (pink). Gentle orange shading signifies second Trump 2.0 administration. Supply: policyuncertainty.com.

For extra on nowcasting commerce utilizing (partially) container visitors, see this blogpost.

Extra precisely, nowcasted utilizing inbound container visitors. Two thirds of Chinese language imports (by worth) comes by sea freight. And sea freight from China doesn’t appear to be rebounding; from Torsten Slok:

Supply: Slok, Might 25, 2025.

How are TEUs correlated with imports? Right here’s whole LA/Lengthy Seashore inbound TEUs and Chinese language imports (deflated into 2003M12$)

Determine 1: Items imports from China, mn 2003M12$, n.s.a (blue, left log scale), crammed inbound TEUs to LA and Lengthy Seashore ports, n.s.a. (tan, proper log scale). Nominal sequence deflated into actual utilizing deflator for imports of Chinese language items. NBER peak-to-trough recession dates shaded grey. Supply: BEA , BLS by way of FRED, Ports of LA, Lengthy Seashore, NBER and creator’s calculations.

Can we predict April imports from China primarily based on inbound TEU’s? Over the 2022M01-2025M03 interval, I estimate in log first variations (utilizing not seasonally adjusted knowledge):

Δimpcht = -0.013 + 0.239 Δteu_LAt + 0.303Δteu_LBt + ut

Adj-R2 = 0.26, SER = 0.086, DW = 2.37, NObs = 39. Daring denotes important at 10% msl, utilizing Newey-West s.e.

Determine 2: Imports from China (black), and predicted imports utilizing indicated equation (mild blue), each in mn.2003M12$. Supply: BEA, BLS by way of FRED, and creator’s calculations.

Ought to we anticipate a rebound now that there’s been an obvious pause in escalation within the commerce warfare with China. The primary determine supplied by Slok suggests no. And given the extremely fickle nature of Trump 2.0 commerce coverage, it’s comprehensible why that is the case.

Determine 3: EPU – commerce class (blue), 7-day centered transferring common (pink). Gentle orange shading signifies second Trump 2.0 administration. Supply: policyuncertainty.com.

For extra on nowcasting commerce utilizing (partially) container visitors, see this blogpost.

{kind=link}