by Calculated Danger on 5/21/2025 01:01:00 PM

Word: This index is a number one indicator primarily for brand spanking new Business Actual Property (CRE) funding.

From the AIA: ABI April 2025: Billings proceed to say no at structure corporations

The AIA/Deltek Structure Billings Index (ABI) rating declined to 43.2 for the month. Billings have declined for 28 of the final 31 months, since they first dipped again into adverse territory following the post-pandemic increase. Regardless of typically sturdy backlogs at corporations, inquiries into new work declined for the third consecutive month in April, whereas the worth of latest design contracts declined on the majority of corporations for the fourteenth consecutive month. Though the U.S. economic system just isn’t formally in a recession at the moment, many structure corporations are reporting recession-like enterprise circumstances.

Regionally, enterprise circumstances at structure corporations remained softest at corporations positioned within the Northeast for the seventh consecutive month in April. Circumstances have additionally softened considerably at corporations positioned within the West for the reason that starting of the 12 months. As well as, billings continued to say no at corporations of all specializations this month, significantly at corporations with business/industrial and multifamily residential specializations. The tempo of the decline stays slower at corporations with an institutional specialization, however billings have nonetheless declined practically each month since mid-2023.

…

The ABI rating is a number one financial indicator of development exercise, offering an roughly nine-to-twelve-month glimpse into the way forward for nonresidential development spending exercise. The rating is derived from a month-to-month survey of structure corporations that measures the change within the variety of companies supplied to purchasers.

emphasis added

• Northeast (40.2); Midwest (44.4); South (46.2); West (42.1)

• Sector index breakdown: business/industrial (40.5); institutional (46.3); multifamily residential (40.8)

Click on on graph for bigger picture.

Click on on graph for bigger picture.

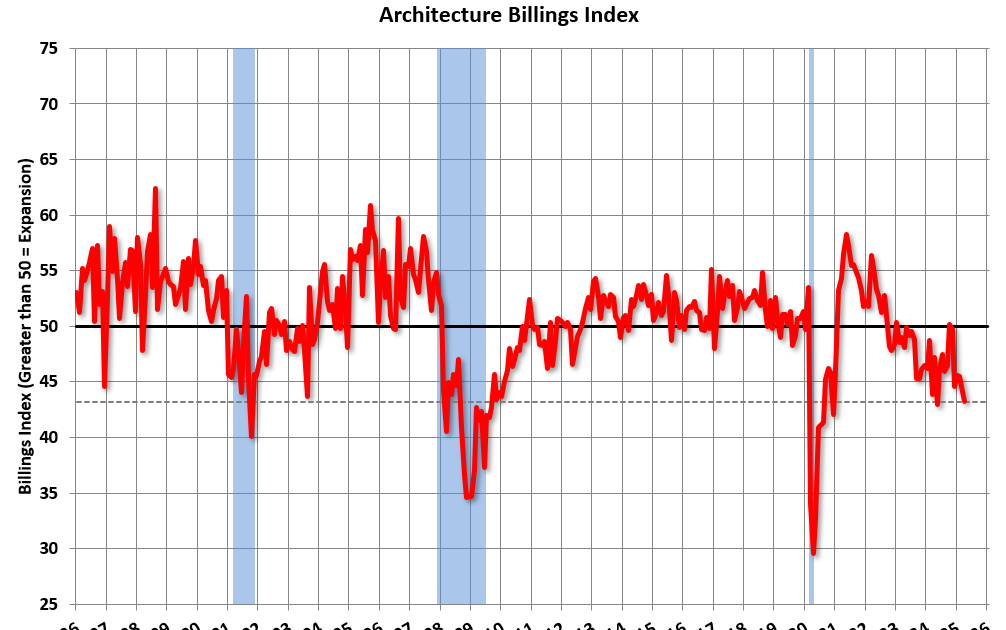

This graph reveals the Structure Billings Index since 1996. The index was at 43.2 in April, down from 44.1 in March. Something under 50 signifies a lower in demand for architects’ companies.

Word: This consists of business and industrial services like inns and workplace buildings, multi-family residential, in addition to colleges, hospitals and different establishments.

This index normally leads CRE funding by 9 to 12 months, so this index suggests a slowdown in CRE funding all through 2025 and into 2026.

Multi-family billings have been under 50 for the 33 consecutive months. This implies we’ll see continued weak spot in multi-family begins.

by Calculated Danger on 5/21/2025 01:01:00 PM

Word: This index is a number one indicator primarily for brand spanking new Business Actual Property (CRE) funding.

From the AIA: ABI April 2025: Billings proceed to say no at structure corporations

The AIA/Deltek Structure Billings Index (ABI) rating declined to 43.2 for the month. Billings have declined for 28 of the final 31 months, since they first dipped again into adverse territory following the post-pandemic increase. Regardless of typically sturdy backlogs at corporations, inquiries into new work declined for the third consecutive month in April, whereas the worth of latest design contracts declined on the majority of corporations for the fourteenth consecutive month. Though the U.S. economic system just isn’t formally in a recession at the moment, many structure corporations are reporting recession-like enterprise circumstances.

Regionally, enterprise circumstances at structure corporations remained softest at corporations positioned within the Northeast for the seventh consecutive month in April. Circumstances have additionally softened considerably at corporations positioned within the West for the reason that starting of the 12 months. As well as, billings continued to say no at corporations of all specializations this month, significantly at corporations with business/industrial and multifamily residential specializations. The tempo of the decline stays slower at corporations with an institutional specialization, however billings have nonetheless declined practically each month since mid-2023.

…

The ABI rating is a number one financial indicator of development exercise, offering an roughly nine-to-twelve-month glimpse into the way forward for nonresidential development spending exercise. The rating is derived from a month-to-month survey of structure corporations that measures the change within the variety of companies supplied to purchasers.

emphasis added

• Northeast (40.2); Midwest (44.4); South (46.2); West (42.1)

• Sector index breakdown: business/industrial (40.5); institutional (46.3); multifamily residential (40.8)

Click on on graph for bigger picture.

This graph reveals the Structure Billings Index since 1996. The index was at 43.2 in April, down from 44.1 in March. Something under 50 signifies a lower in demand for architects’ companies.

Word: This consists of business and industrial services like inns and workplace buildings, multi-family residential, in addition to colleges, hospitals and different establishments.

This index normally leads CRE funding by 9 to 12 months, so this index suggests a slowdown in CRE funding all through 2025 and into 2026.

Multi-family billings have been under 50 for the 33 consecutive months. This implies we’ll see continued weak spot in multi-family begins.

by Calculated Danger on 5/21/2025 01:01:00 PM

Word: This index is a number one indicator primarily for brand spanking new Business Actual Property (CRE) funding.

From the AIA: ABI April 2025: Billings proceed to say no at structure corporations

The AIA/Deltek Structure Billings Index (ABI) rating declined to 43.2 for the month. Billings have declined for 28 of the final 31 months, since they first dipped again into adverse territory following the post-pandemic increase. Regardless of typically sturdy backlogs at corporations, inquiries into new work declined for the third consecutive month in April, whereas the worth of latest design contracts declined on the majority of corporations for the fourteenth consecutive month. Though the U.S. economic system just isn’t formally in a recession at the moment, many structure corporations are reporting recession-like enterprise circumstances.

Regionally, enterprise circumstances at structure corporations remained softest at corporations positioned within the Northeast for the seventh consecutive month in April. Circumstances have additionally softened considerably at corporations positioned within the West for the reason that starting of the 12 months. As well as, billings continued to say no at corporations of all specializations this month, significantly at corporations with business/industrial and multifamily residential specializations. The tempo of the decline stays slower at corporations with an institutional specialization, however billings have nonetheless declined practically each month since mid-2023.

…

The ABI rating is a number one financial indicator of development exercise, offering an roughly nine-to-twelve-month glimpse into the way forward for nonresidential development spending exercise. The rating is derived from a month-to-month survey of structure corporations that measures the change within the variety of companies supplied to purchasers.

emphasis added

• Northeast (40.2); Midwest (44.4); South (46.2); West (42.1)

• Sector index breakdown: business/industrial (40.5); institutional (46.3); multifamily residential (40.8)

Click on on graph for bigger picture.

This graph reveals the Structure Billings Index since 1996. The index was at 43.2 in April, down from 44.1 in March. Something under 50 signifies a lower in demand for architects’ companies.

Word: This consists of business and industrial services like inns and workplace buildings, multi-family residential, in addition to colleges, hospitals and different establishments.

This index normally leads CRE funding by 9 to 12 months, so this index suggests a slowdown in CRE funding all through 2025 and into 2026.

Multi-family billings have been under 50 for the 33 consecutive months. This implies we’ll see continued weak spot in multi-family begins.

by Calculated Danger on 5/21/2025 01:01:00 PM

Word: This index is a number one indicator primarily for brand spanking new Business Actual Property (CRE) funding.

From the AIA: ABI April 2025: Billings proceed to say no at structure corporations

The AIA/Deltek Structure Billings Index (ABI) rating declined to 43.2 for the month. Billings have declined for 28 of the final 31 months, since they first dipped again into adverse territory following the post-pandemic increase. Regardless of typically sturdy backlogs at corporations, inquiries into new work declined for the third consecutive month in April, whereas the worth of latest design contracts declined on the majority of corporations for the fourteenth consecutive month. Though the U.S. economic system just isn’t formally in a recession at the moment, many structure corporations are reporting recession-like enterprise circumstances.

Regionally, enterprise circumstances at structure corporations remained softest at corporations positioned within the Northeast for the seventh consecutive month in April. Circumstances have additionally softened considerably at corporations positioned within the West for the reason that starting of the 12 months. As well as, billings continued to say no at corporations of all specializations this month, significantly at corporations with business/industrial and multifamily residential specializations. The tempo of the decline stays slower at corporations with an institutional specialization, however billings have nonetheless declined practically each month since mid-2023.

…

The ABI rating is a number one financial indicator of development exercise, offering an roughly nine-to-twelve-month glimpse into the way forward for nonresidential development spending exercise. The rating is derived from a month-to-month survey of structure corporations that measures the change within the variety of companies supplied to purchasers.

emphasis added

• Northeast (40.2); Midwest (44.4); South (46.2); West (42.1)

• Sector index breakdown: business/industrial (40.5); institutional (46.3); multifamily residential (40.8)

Click on on graph for bigger picture.

This graph reveals the Structure Billings Index since 1996. The index was at 43.2 in April, down from 44.1 in March. Something under 50 signifies a lower in demand for architects’ companies.

Word: This consists of business and industrial services like inns and workplace buildings, multi-family residential, in addition to colleges, hospitals and different establishments.

This index normally leads CRE funding by 9 to 12 months, so this index suggests a slowdown in CRE funding all through 2025 and into 2026.

Multi-family billings have been under 50 for the 33 consecutive months. This implies we’ll see continued weak spot in multi-family begins.

{kind=link}